Every month I get the same question: "Are rates going up or down?" And every month I tell people that's the wrong question. The number on the screen is the result. What you want to know is why it moved and what's loaded for next month. So let's do that.

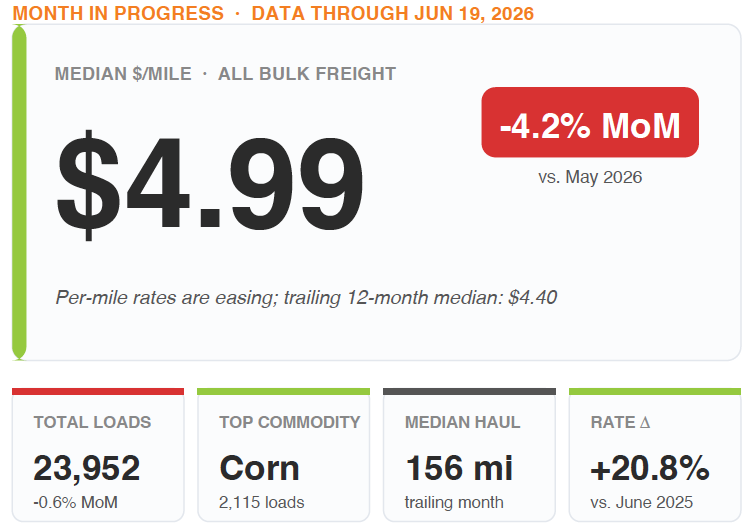

The blended median eased to $4.99 a mile, down 4.2% from May. Stop there and you'd think the market is rolling over. It isn't. That same $4.99 is up 20.8% against June of last year, and the freight that actually moves this network firmed up underneath the average.

Here's the why behind the dip:

- Grain rates rose about 9% on the month and aggregates gained about 8%. Every major group climbed. The blended median fell anyway because the load mix tilted toward shorter, lower-rate lanes. That's a mix story, not a weakness story.

- Volume held flat. Loads came in just 0.6% under May and are running 8.5% above the trailing 12-month average. Demand is ahead of the seasonal trend, not behind it.

- Short-haul still owns the map. The top three corridors moved 20% of all flow, and grain is 34% of the mix.

Corn is carrying the network

BulkLoads verified carrier submissions · 2,115 Corn loads in June 2026.

Corn was the single highest-volume product we verified this month at 2,115 loads, up 8.3% on the month and 30% on the year. When the most-hauled commodity in the network is climbing while the blended average eases, that's the tell. Old-crop corn is moving out of storage ahead of new crop, feed and ethanol demand held, and the lanes that carry it are tight. Watch corn as your leading indicator into harvest.

The one that decides Q3: diesel, and a truce that's doing the work

EIA Weekly Retail On-Highway Diesel Prices · Latest reading: June 15, 2026 · PADDs: R10 East Coast / R20 Midwest / R30 Gulf / R40 Rocky Mountain / R50 West Coast.

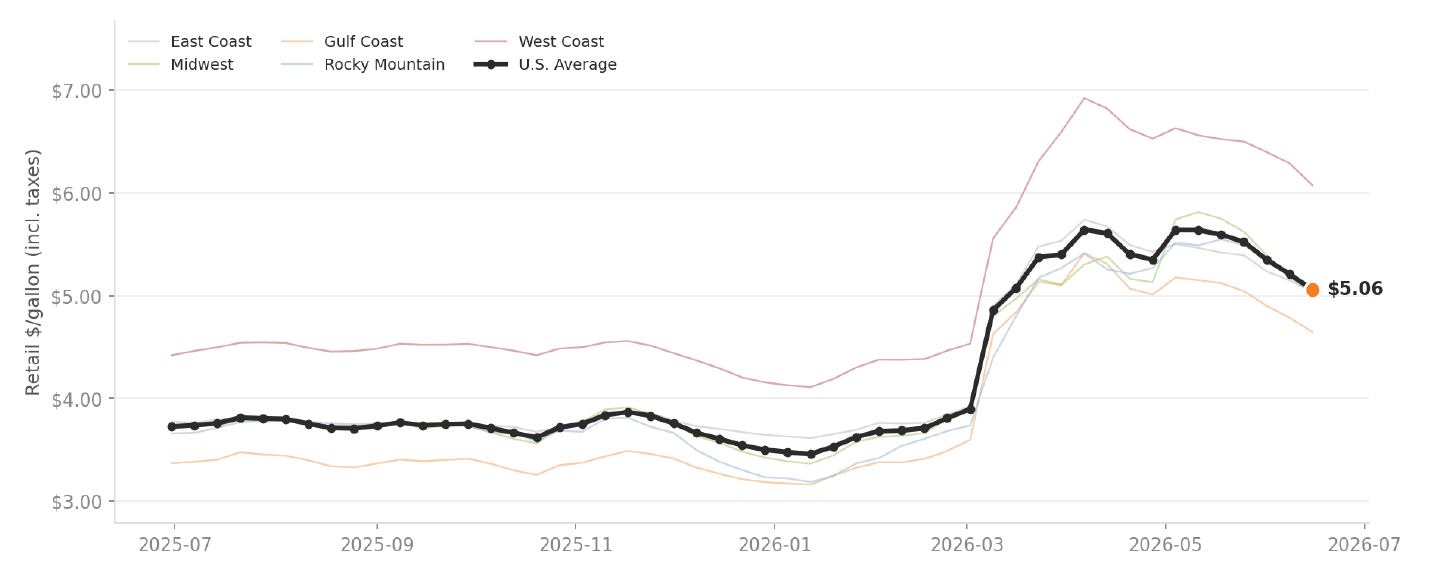

This is the chart I'd tape to your wall. The US average dropped to $5.06 a gallon, down 9.6% on the month and now basically flat over the trailing three. That 12-month spike was the Iran conflict pulling barrels off the water and resetting the entire diesel curve higher, which is the real reason your rate floor still sits 20% above last June.

Now here's what changed. A preliminary ceasefire framework and a 60-day negotiating window have already pulled diesel about 50 cents off its mid-May level. Right now, the fuel side is doing the work for carriers. That is the single most direct tailwind on this report.

But read the next part carefully, because most people will get it wrong: this is not a settled deal. Nuclear terms and the actual reopening of the Strait of Hormuz are still unresolved, and the framework has already been tested. So treat the relief as real but reversible:

- Near term: the fuel tailwind is genuine and it's helping your margins today.

- If the framework holds: diesel grinds lower and rate floors ease with it over Q3 and Q4.

- If it breaks down: fuel snaps back upward fast, and your rate floor follows. This is a watch item, not a victory lap.

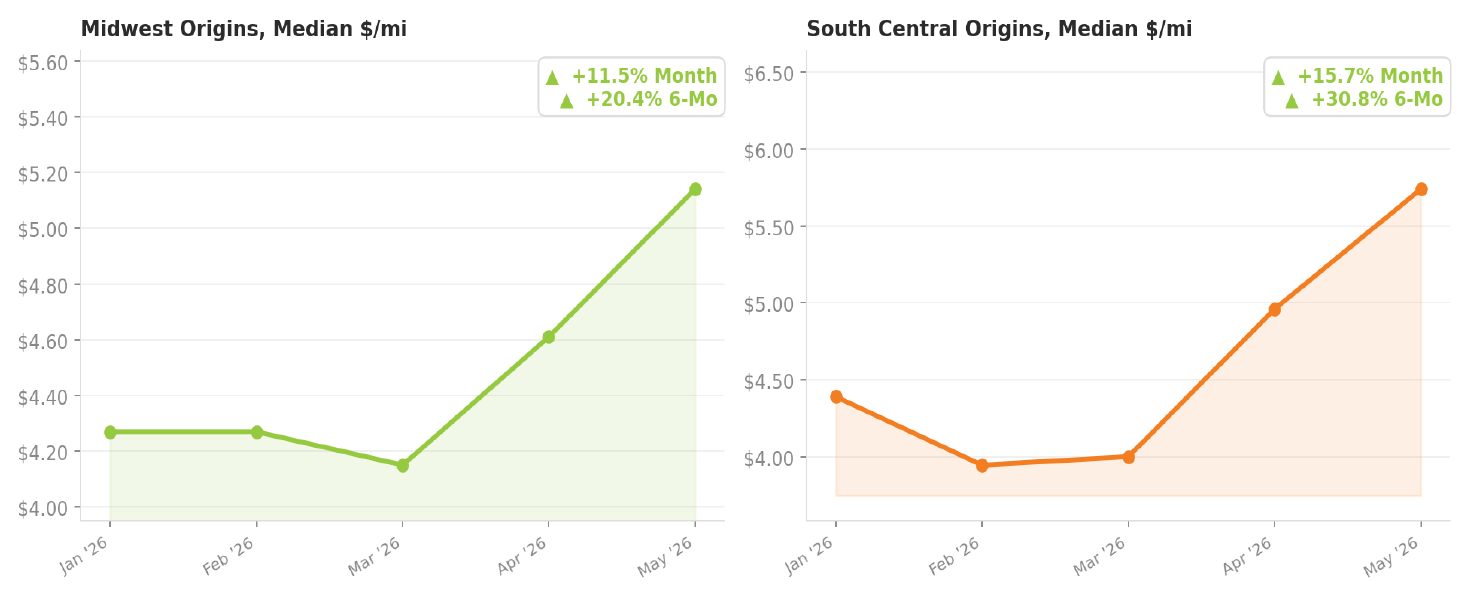

The regional split is shifting

Median per-mile rates for loads originating in each region over the trailing 6 months. Midwest = corn-belt grain states (IA, IL, IN, OH, MI, WI, MN, MO, KS, NE, SD, ND). South Central = TX, OK, NM.

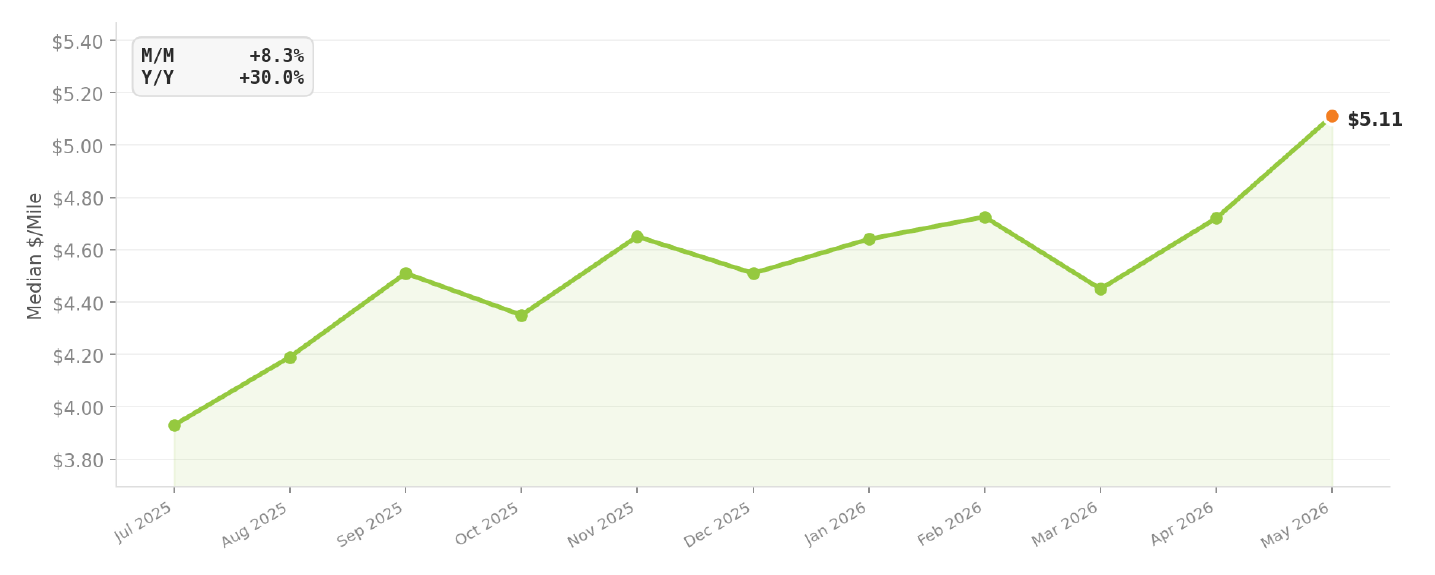

The six-month trend has both the Midwest and South Central up big, but the month-to-date read is splitting them. The Midwest is the strongest place to be. South Central, after a huge run, cooled 6.8% this month, and the Northeast firmed +3.9%. If you run grain-belt lanes, you're in the strong part of the market. If you lean South Central, this is the month it gave a little back.

What I'd watch into July

- Diesel and the truce. The fuel tailwind is real, but it's resting on a fragile framework. Track it weekly.

- Corn and the harvest setup. The bellwether is rising against the season. Bullish for grain lanes into fall.

- The Midwest holding while South Central cools. Lane selection matters more this month than last.

The carriers and shippers who win the next two quarters won't react to last month's number. They'll price the fuel move while it's still moving.

That's what we built BulkLoads Insights to do: real-time rate quoting by lane and commodity, fuel-adjusted estimates that move with the diesel curve, and verified, transaction-backed data behind every number here. Bring your toughest lane and book a 30-minute walkthrough with me at bulkloads.com/bulk-insights/. I'll show you the data.

John F. Calloway · Growth Architect, Enterprise · [email protected] · (417) 501-3934