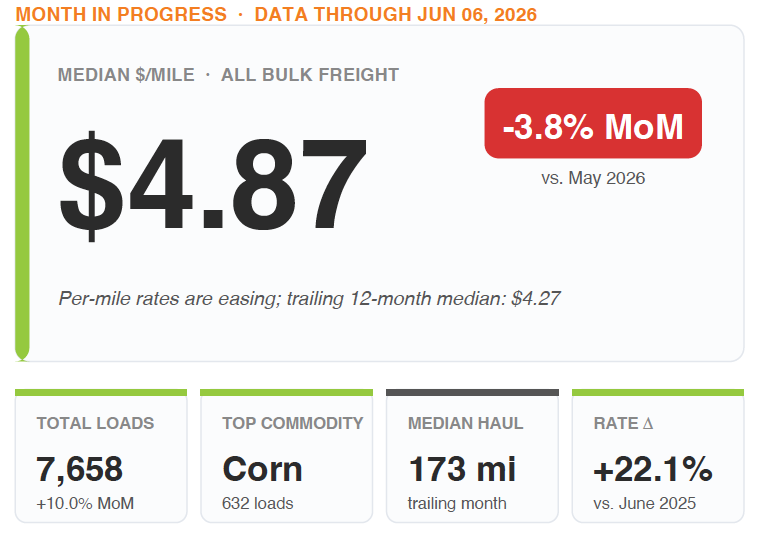

We're about a week into June, and the headline number is going to fool a lot of people. Rates across all bulk freight eased about 3.8% versus the same stretch of May, down to a median of $4.87 per mile. On paper that looks like the market cooled off.

It didn't. That same $4.87 is up 22% versus last June, and it is still sitting well above our trailing 12-month median of $4.27. Most of the monthly dip is a fuel story, not a demand story, and once you understand what moved diesel, the rest of the month makes a lot more sense. Let me walk through it.

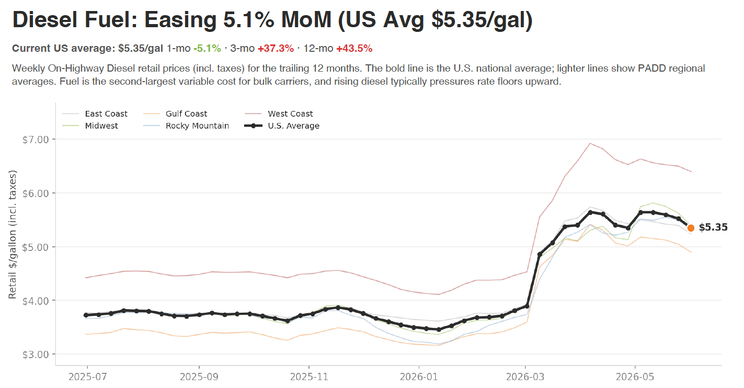

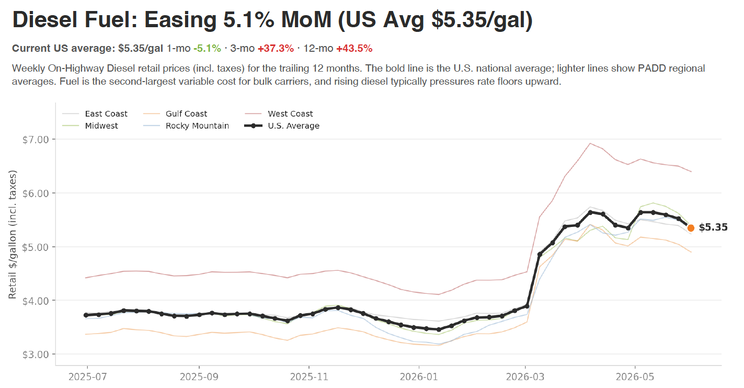

First, Why Rates Eased: Diesel Finally Cracked

If you fuel a truck, you already felt this. The national average for on-highway diesel came in at $5.35 a gallon to start June, down better than 5% on the month. After the spring we just had, take the win.

Here is the backstory, because it matters. Diesel ran to multi-year highs earlier this year after conflict in the Middle East choked off a chunk of global oil flow. The EIA had crude spiking and diesel pushing past $5.40 a gallon this spring, the highest in real terms in over two years. What changed in the last few weeks is the risk premium coming back out. Peace and ceasefire talk in the region, plus Middle East production recovering, pulled crude back down hard (WTI dropped roughly nine dollars a barrel in a single week into late May), and diesel followed it lower.

Now connect that to your rate. A big piece of any bulk rate is the fuel component. When diesel falls this fast, rate floors ease right along with it. That is most of your 3.8% monthly dip. It is not shippers deciding freight is suddenly worth less. It is fuel coming off a spike. And keep it in context: diesel is still better than 40% higher than it was a year ago, which is exactly why rates have held up the way they have all year.

EIA Weekly Retail On-Highway Diesel Prices · Latest reading: June 01, 2026 · PADDs: R10 East Coast / R20 Midwest / R30 Gulf / R40 Rocky Mountain / R50 West Coast.

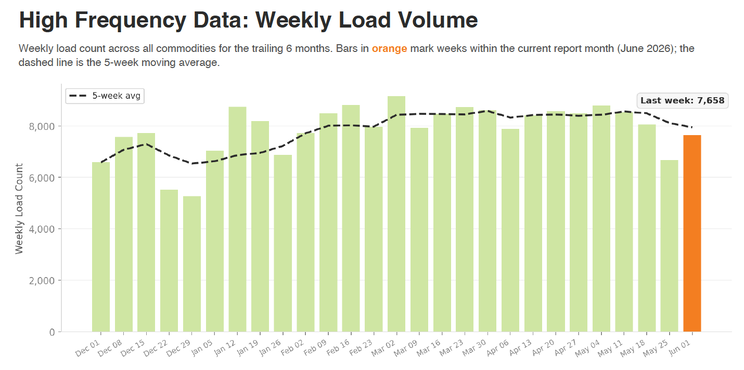

Underneath the Fuel Move, the Freight Market Is on Fire

Strip the fuel noise out and the demand picture is strong, and not just in bulk. The broader spot market is running at levels we have not seen since the 2021 and 2022 boom. FTR has total spot loads in 2026 tracking dramatically above both 2025 and 2024, with dry van rates near record territory and flatbed posting outright records. The reason is years in the making. Carriers exited through 2024 and 2025, capacity got thin, and now demand is bumping into a smaller truck pool.

Our own network is telling the same story. Loads through the first six days of June came in at 7,658, up 10% against the same window in May, and running roughly 18.6% above our trailing 12-month average for this point in the month. When volume runs that far ahead of trend while rates only ease a few points on falling fuel, that is a market with its foot still on the gas.

BulkLoads verified carrier submissions, weekly aggregates.

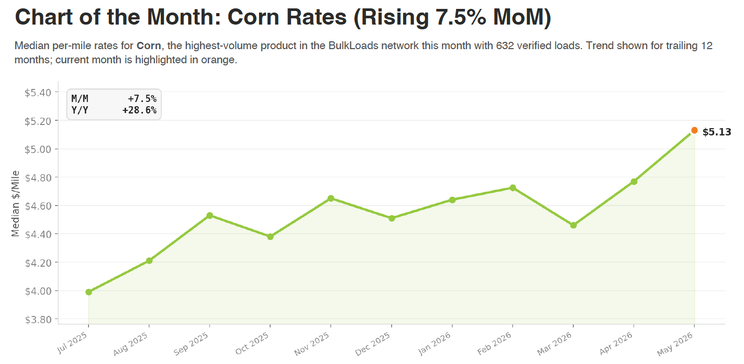

The Corn Story That Trips Everybody Up

Here is the one I want you to read twice, because the headline and the freight go opposite directions.

If you follow the futures board, you know corn prices have been falling. Corn slid to seven-week lows in early June, down near $4.40 a bushel, on benign Midwest weather, expectations for another huge crop, soft export sales, and money managers selling. Falling crude added to the pressure. So why did corn freight rates in our network climb 7.5% on the month, to a median of $5.13 a mile, with corn the single highest-volume product we moved?

Because freight does not pay for the price of the corn. It pays for moving it. And right now there is a mountain of it to move. The last harvest was a record, old-crop inventories are large, and elevators are clearing space ahead of the next crop. Low prices actually speed that up. Cheap corn moves to ethanol plants, feedlots, and export terminals, and it moves by truck on the front end. So a soft futures board and strong corn freight are not a contradiction. They are the same oversupplied market seen from two different seats. If your equipment fits grain, the back half of this season is setting up with freight, not without it.

BulkLoads verified carrier submissions · 632 Corn loads in June 2026.

The Money Is Moving Short and Regional

The median haul in June so far is 173 miles. Short. And the three busiest corridors in the entire network were all intrastate. Oklahoma to Oklahoma led at 496 loads, Kansas to Kansas followed at 445, and Texas to Texas at 413. Those three lanes alone were 18% of all flow.

That is partly structural and partly seasonal. On the structural side, a lot of carriers spent the last two years pulling out of long-haul and rebuilding around regional lanes, and you can see it in the data, with short-haul and long-haul rates behaving very differently. On the seasonal side, grain is moving locally to elevators and processors, and winter wheat harvest is just kicking off across the southern Plains. The takeaway for you is simple. If you have been chasing long pulls and eating deadhead to get home, the math this month may favor running denser and shorter and staying loaded. More loaded miles at four-plus a mile beats one long haul with an empty backhaul.

Where Rates Are Firming, and Where They're Not

The clear regional winner this month is the South Central, Texas, Oklahoma, and New Mexico, up almost 16% on the month and better than 30% over six months. There is a lot stacked up behind that. Winter wheat harvest is starting in the hard red winter belt. Cattle and feed freight is active. And the data center construction wave across Texas and Oklahoma keeps pulling in building materials, steel, and aggregates. Nonresidential construction tied to the AI buildout is running near $50 billion annualized right now, and a single data center can absorb tens of thousands of truckloads of material.

The Midwest firmed too, up around 8.6%, on all that grain movement. The Northeast quietly strengthened by 5.5%.

The soft spot is the West, down about 11%. A big piece of that is trade. After the early-year rush to bring imports in ahead of tariffs, import volumes have pulled back sharply, and that hits the port-adjacent western markets first. Wheat was the weakest single product, off about 11%, as harvest pressure, drought relief in the growing regions, and trade uncertainty with China pushed wheat values to one-month lows.

Median per-mile rates for loads originating in each region over the trailing 6 months. Midwest = corn-belt grain states (IA, IL, IN, OH, MI, WI, MN, MO, KS, NE, SD, ND). South Central = TX, OK, NM.

A Note on Aggregates and Coal

Aggregates and Industrial cooled this month, with rates off about 2.5% and the group giving back a little share. I am not reading much into one soft month. The longer-term demand picture for aggregates, driven by that data center pipeline, has not changed, and housing-related material freight is the part that is genuinely subdued right now, held back by high mortgage rates and elevated inventory. I will be watching whether aggregates firm back up as construction season hits full stride.

On the other end, coal was actually the strongest single-product rate move of the month, up 5.7%. That is a seasonal power-demand story. A hot start to summer pulls generation up, and coal freight moves with it.

What I'd Be Watching Into Late June

A few things on my radar as the month fills in. Whether diesel keeps easing or the Middle East risk premium snaps back, because that is your rate floor. Whether corn and grain hold their freight strength as harvest volume builds. Whether the West stabilizes or keeps sliding on the import pullback. And whether that short-haul, regional concentration holds, because if it does, your routing plan for the next 30 days should reflect it.

Want This for Your Own Lanes?

Everything here is the network average. Your trucks do not run the average. They run specific lanes.

If you want to see what your exact lanes are paying right now, fuel-adjusted, with a confidence score behind every number, that is what Bulk Insights does. It is the live, interactive version of this report.

I do 30-minute walkthroughs with carriers, brokers, and shippers every week. If you want to see whether it fits your operation, grab a slot at bulkfreightinsights.com ↗ or reach me directly at [email protected].

Either way, keep moving freight, watch the fuel, and let's see what the rest of June brings.