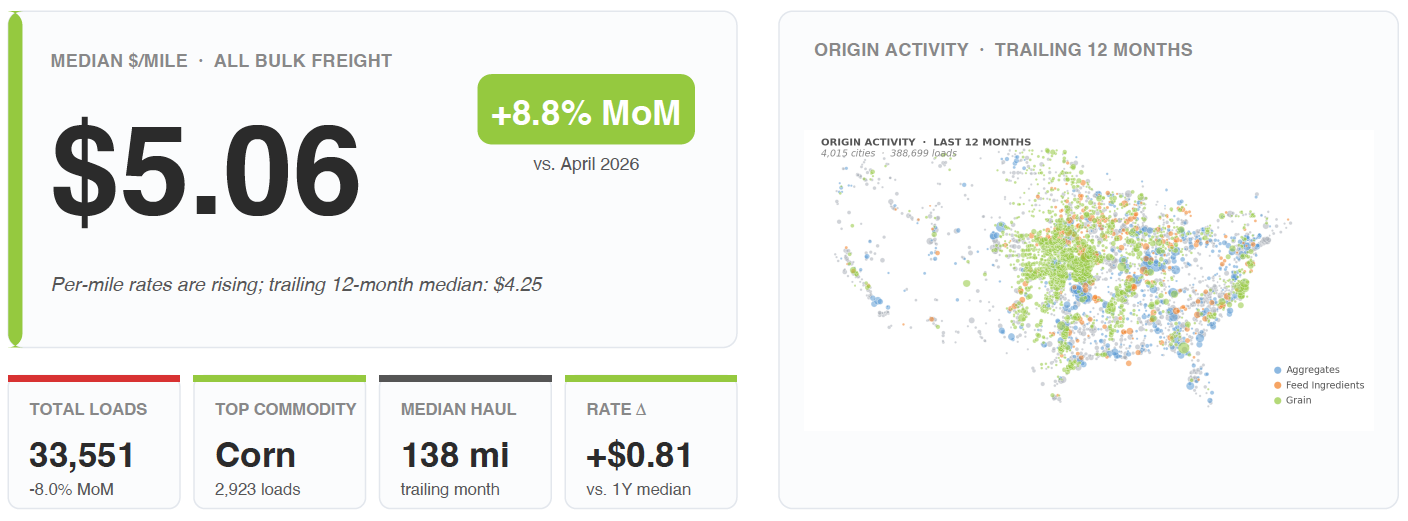

May wrapped up with bulk freight clearly in shift mode. The median rate landed at $5.06 per mile across 33,551 verified loads, up 8.8% from April and sitting $0.81 above the trailing 12-month median.

Volume told a different story. Total loads came in 8.0% below April. That gap between rising rates and falling volume is the part worth paying attention to. When less freight is moving and it's pricing higher, capacity is tightening faster than demand is fading. That doesn't usually reverse overnight.

A Few Quick Stats From the Month

- Corn was the volume leader with 2,923 loads, the single biggest product in our network

- Median haul came in at 138 miles, reinforcing how short-haul this market has become

- The top three corridors (OK to OK, KS to KS, IN to IN) accounted for 21% of all flow

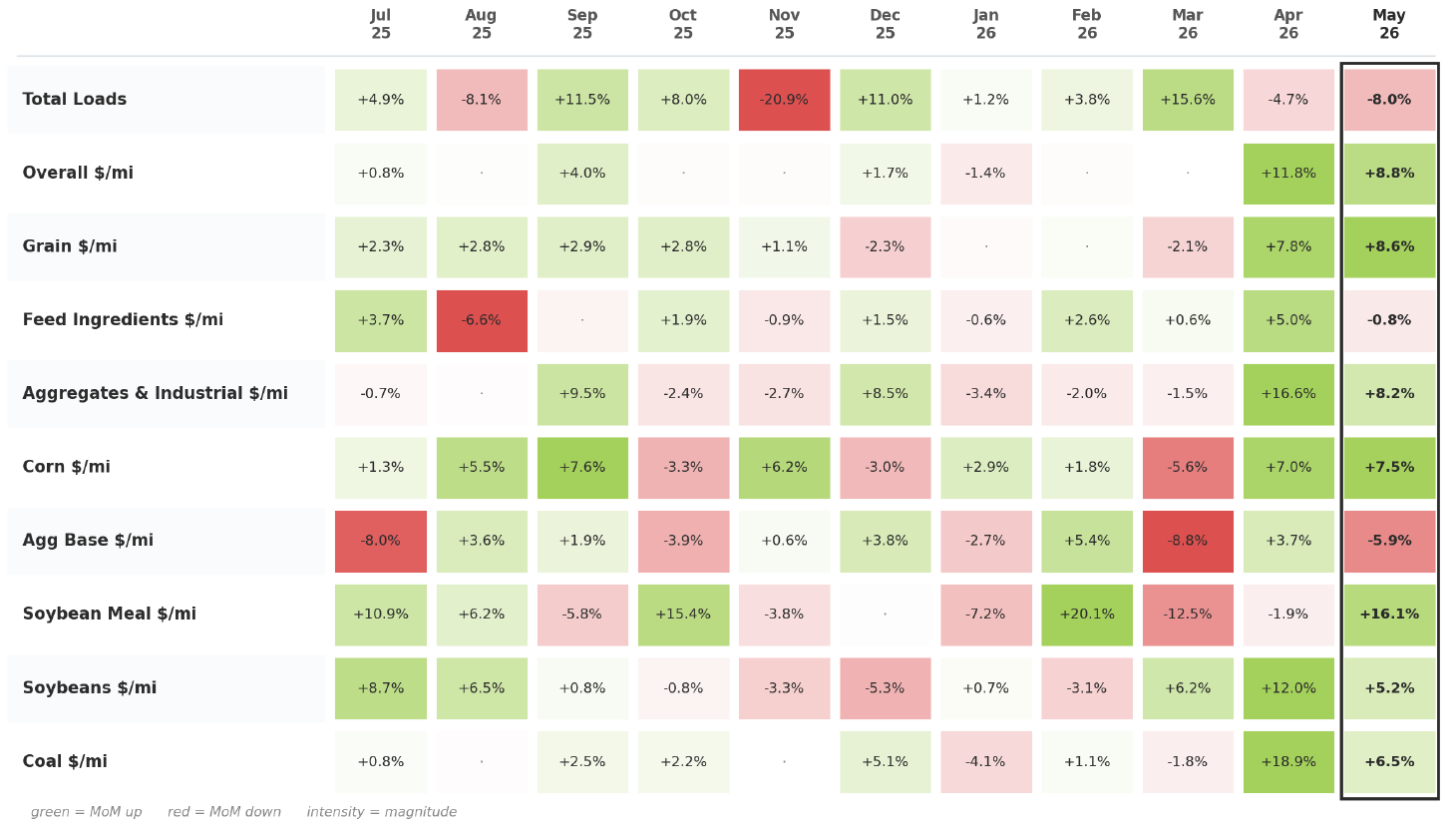

What the 12-Month Picture Shows

Looking back across the full 12-month window, almost every row finished green in May. Corn finished +7.5%, Soybean Meal jumped +16.1%, Coal climbed +6.5%, and Grain as a category landed at +8.6%. The standout red is Agg Base at -5.9%, which I'll come back to in a second.

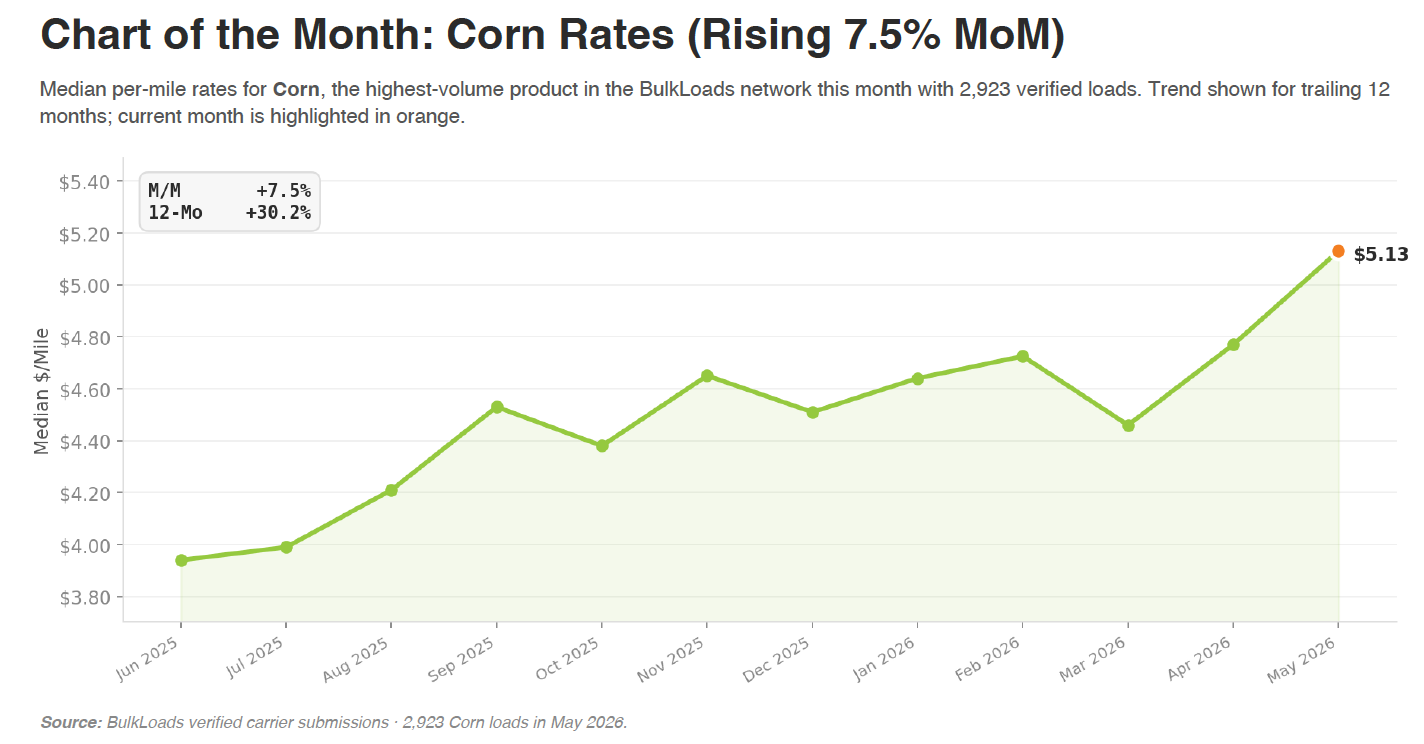

Corn Deserves a Closer Look

As the highest-volume product on the platform this month, corn's per-mile rate finished at $5.13 — up 7.5% MoM and 30.2% over the trailing 12 months. When your biggest commodity by volume is also pulling rates upward at that pace, it tends to drag adjacent products with it. Watch this one through the summer.

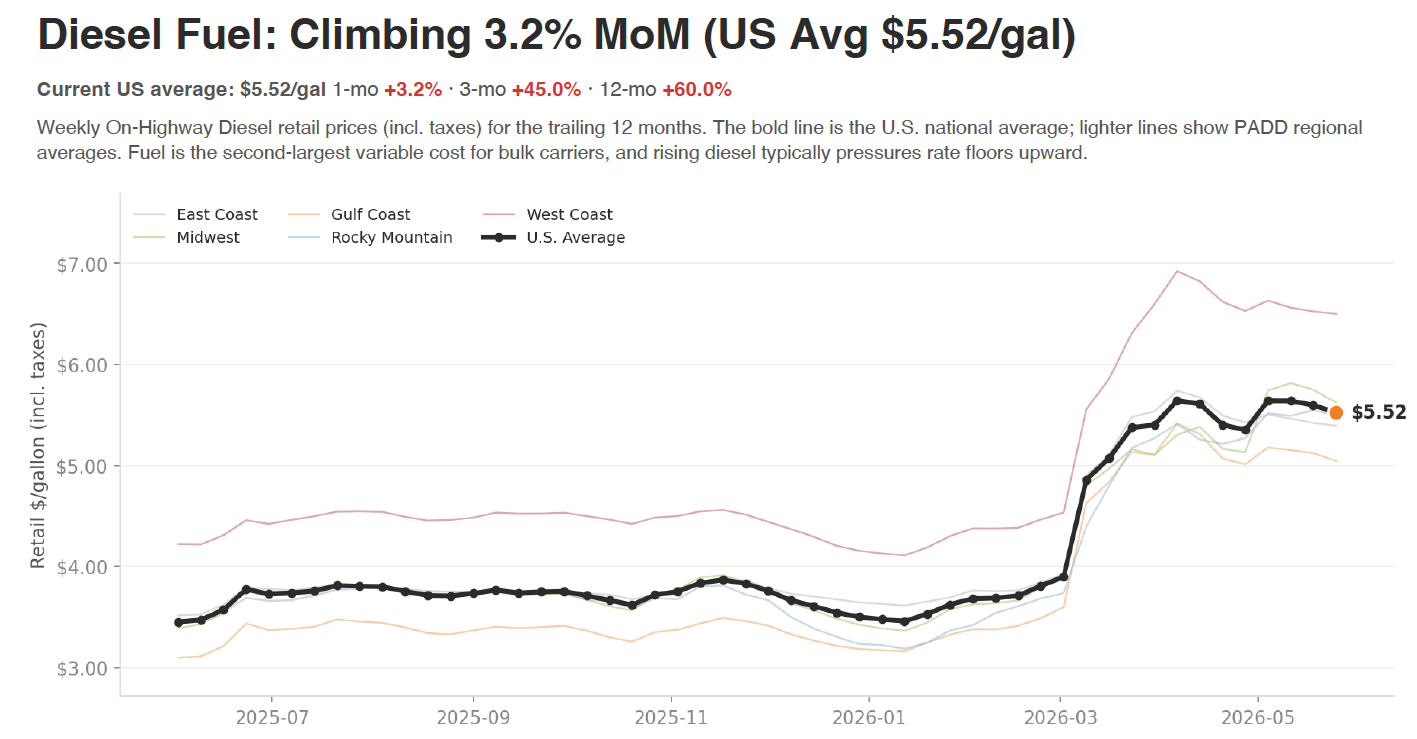

The Fuel Side Isn't Helping Carriers Breathe

The U.S. average for on-highway diesel sits at $5.52 per gallon. That's up 3.2% this month, 45% over three months, and 60% year over year. Fuel is the second-largest variable cost we track, and when diesel runs this hot, rate floors have nowhere to go but up.

How the Wins and Losses Stacked Up

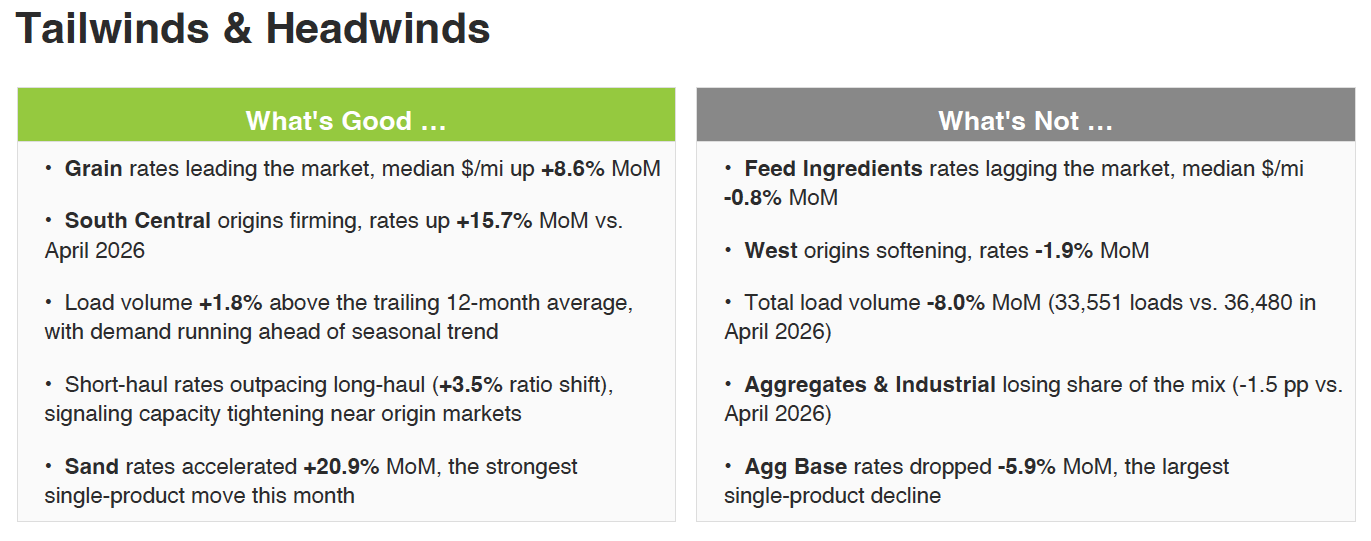

On the positive side, Grain led the market, South Central origins firmed 15.7% (up 44.2% over six months — a number that's hard to ignore), and Sand rates posted the strongest single-product move at +20.9%. Short-haul rates outpacing long-haul by 3.5% points to continued tightness near origin markets.

On the other side, Feed Ingredients slipped 0.8%, West origins cooled 1.9%, Aggregates lost 1.5 points of mix share, and Agg Base gave back 5.9%.

What This Means If You're Booking Freight Right Now

Pricing power has shifted. The lanes you ran in March or April are not the same lanes today, and walking into a quote with stale numbers is leaving real money on the table whether you're shipping or hauling.

If you want more than a monthly snapshot, BulkLoads Insights ↗ gives you live rate-quoting, lane analysis, and fuel-adjusted estimates for every commodity we cover.